Sorry, but your login has failed. Please recheck your login information and resubmit. If your subscription has expired, renew here.

March-April 2026

The March/April 2026 issue of Supply Chain Management Review examines how supply chain leaders are managing supplier risk, circular supply chain design, AI-driven retail planning, CPG network optimization, and shifting LTL market dynamics to improve resilience and performance. Features include frameworks to prevent supplier failure, operationalize circular economy strategies, prevent retail stockouts using AI, and eliminate costly DC transfer patterns, plus insights from the 34th Annual Study of Logistics and Transportation Trends and a digital-exclusive on the evolving CSCO role. Browse this issue archive.Need Help? Contact customer service 1-508-503-1313 More options

Corporate climate credibility increasingly hinges on Scope 3 emissions, and yet individual companies have the least direct control over these emissions. Meeting ambitious Scope 3 targets requires industry level collaboration that rewires incentives, standardizes expectations, and lowers the cost of decarbonization, especially now that turbulent climate, trade, and tariff policies can abruptly change the economics of low carbon supply choices. Policy and tariff volatility does not simply increase costs; more widely, it disrupts sourcing strategies and undermines long term decarbonization pathways by constraining access to low carbon inputs.

SC

MR

Sorry, but your login has failed. Please recheck your login information and resubmit. If your subscription has expired, renew here.

March-April 2026

The March/April 2026 issue of Supply Chain Management Review examines how supply chain leaders are managing supplier risk, circular supply chain design, AI-driven retail planning, CPG network optimization, and… Browse this issue archive. Access your online digital edition. Download a PDF file of the March-April 2026 issue.Corporate climate credibility increasingly hinges on Scope 3 emissions, and yet individual companies have the least direct control over these emissions. Meeting ambitious Scope 3 targets requires industry‑level collaboration that rewires incentives, standardizes expectations, and lowers the cost of decarbonization, especially now that turbulent climate, trade, and tariff policies can abruptly change the economics of low‑carbon supply choices. Policy and tariff volatility does not simply increase costs; more widely, it disrupts sourcing strategies and undermines long‑term decarbonization pathways by constraining access to low‑carbon inputs.

Scope 3: Where the footprint really sits

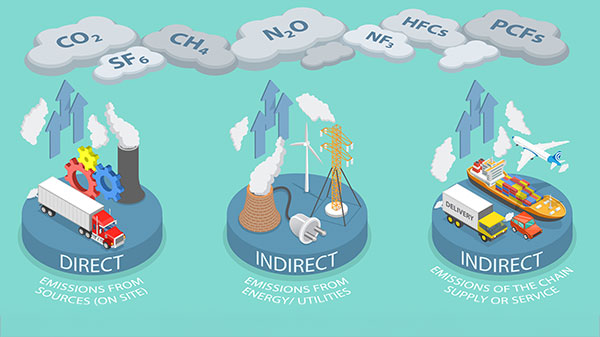

For most companies, the majority of greenhouse gas emissions do not come from their own operations or purchased energy. Instead, they sit upstream and downstream in the value chain, embedded in purchased goods, supplier manufacturing, transportation, and distribution. These indirect emissions, known as Scope 3, typically account for around 75% of a company’s total carbon footprint, according to CDP Worldwide Technical Note: Relevance of Scope 3 Categories by Sector (version 3.0).

Over the past decade, many organizations have made steady progress on Scope 1 and Scope 2 emissions. They have improved energy efficiency, shifted to renewable electricity, and optimized their own operations. Scope 3 emissions, however, present a fundamentally different challenge: they span thousands of suppliers, multiple tiers, and diverse geographies. This remains a persistent blind spot amid mounting regulatory pressure from the EU Corporate Sustainability Reporting Directive (CSRD), and investor demands via the Carbon Disclosure Project (CDP) and the Science Based Targets initiative (SBTi). The result is a paradox: Scope 3 emissions matter most, but individual firms have the least visibility and leverage over them. Breaking this paradox requires treating Scope 3 emissions as a systems problem—one that no company can solve in isolation.

Why measuring Scope 3 emissions is so difficult

Across industries, the most frequently cited challenge in measuring Scope 3 emissions is the lack of supplier data. This forces companies to rely on imprecise spend-based estimates that mechanically link emissions to expenditure levels, overstating emissions for high-spend but low-intensity categories and substantially understating emissions for high-intensity categories. Methodological inconsistencies further complicate this, particularly the absence of standardized approaches and the complexity of calculating emissions across global supply chains. Companies must choose between spend-based estimates, supplier-specific data, or industry averages, often applying different approaches across categories and regions. Without widely adopted standards, results are difficult to compare across firms or over time.

Capability gaps further slow progress, ranging from limited internal expertise and high software costs to concerns around data privacy. In practice, many organizations still rely on spreadsheets to manage Scope 3 data. While spreadsheets may be useful for initial reporting, they do not scale to complex global supply chains or support continuous improvement. Together, these constraints mean that even highly motivated firms struggle to establish reliable Scope 3 emissions baselines.

Why reducing Scope 3 is even harder

Measuring Scope 3 is only the first hurdle. Turning numbers into meaningful reductions is often more challenging, even for companies that understand where their emissions are concentrated. The most frequently cited barrier to Scope 3 reduction is a weak business case. Many corporate investment decisions are evaluated on relatively short horizons, yet the benefits of upstream decarbonization (improved data transparency, greater investor confidence, and reputational gains) often accrue over longer periods. This conflict mirrors the difficulty of justifying investments in supply chain resilience: the payoffs are significant,

but they arrive unevenly and prove difficult to capture in a traditional business case, making capital-intensive decarbonization projects difficult to justify. High implementation costs reinforce that perception, especially in sectors where margins are thin and payback periods are long.

Lack of aligned incentives is another constraint. When sustainability requirements are fragmented across buyers, each buyer sends unique questionnaires, sets different thresholds, and requests bespoke data formats, leaving suppliers to navigate a tangle of overlapping and sometimes conflicting requests. Responding becomes administratively expensive, leaving fewer resources for actual emissions reductions. At the same time, if no buyer offers credible long‑term demand or cost‑sharing, suppliers have little incentive to move first on capital‑intensive decarbonization projects. Trade and tariff volatility tilts buyer priorities further toward short-term costs and political risk management, encouraging sourcing decisions that favor price stability or tariff avoidance over emissions performance.

Regulatory uncertainty further complicates planning. While disclosure requirements are expanding, companies remain unsure how rules will evolve, which methodologies will prevail, and how data will be verified. Such uncertainty discourages long-term investment and results in many firms carrying the accountability for Scope 3 targets without clear levers to meet them. This dynamic reveals a central truth about Scope 3: no single company can realistically train, fund, and decarbonize its entire supplier base on its own.

Recognizing these constraints, companies have increasingly turned to supplier engagement as a lever for Scope 3 reduction. Common approaches, such as incorporating sustainability criteria into supplier selection, requesting emissions data, offering training, and requiring third-party audits or certifications, are necessary, but they often rely on foundational procurement levers rather than stronger commercial mechanisms. Long-term contracts tied to sustainability performance, financial incentives, or shared investment models remain underused, leaving even well-designed programs to struggle to scale in isolation. Ultimately, without broader industry alignment, a supplier that invests to meet one buyer’s requirements may see little reward if other buyers do not value those efforts.

How industry collaboration changes the game

Industry collaboration can turn this coordination failure into a shared opportunity. When companies work together by standardizing expectations, pooling demand, and sharing resources, they lower the cost and risk of decarbonization for everyone. The 2025 State of Supply Chain Sustainability Report (https://sustainable.mit.edu/sscs-report/) shows that 87% of companies participating in industry collaborations to track and reduce Scope 3 emissions reported concrete benefits such as stronger supplier engagement, better alignment on sustainability goals, and improved access to emissions data and reporting frameworks. In addition, 64% pointed to benefits from pooled expertise and shared resources, including tangible cost savings from joint sustainability investments.

There are already examples of industry collaboration across and within sectors addressing sustainability challenges, though not specific to Scope 3 emissions. The Better Cotton Initiative (BCI) coordinates farmers, brands, retailers, and NGOs around shared sustainability standards in cotton production, covering water use, chemical inputs, and labor practices. Standardized reporting and verification reduce duplication and enable sustainability improvements at scale. In maritime shipping, the Clean Cargo initiative, hosted by the Smart Freight Centre, is a leading multi-stakeholder partnership supporting the decarbonization of ocean freight, bringing together shippers, carriers, and freight forwarders. This enables a standardized data exchange and standard carbon performance metrics across the industry. With a common methodology for emissions reporting, customers and carriers work together on low-emission freight procurement and supply chain visibility. Similarly, the Responsible Business Alliance (RBA) has established widely adopted standards for labor, environmental practices, and energy use across electronics and tech supply chains. These shared frameworks simplify audits, reduce redundancy, and improve compliance among global suppliers.

More recently, the Scope 3 Emissions Consortium (STEC), launched by the MIT Sustainable Supply Chain Lab, aims to unite companies, technology providers, and researchers to tackle Scope 3 challenges through collective innovation (https://sustainable.mit.edu/stec/). The consortium focuses on harmonizing data standards, building practical tools to support emissions measurement, and creating approaches to help companies better engage suppliers and scale reduction efforts across their value chains.

Turning collaboration into a strategy

For leaders responsible for Scope 3 targets, the question is no longer whether to collaborate, but how. At the company level, the starting point is clarity: identify the major Scope 3 hotspots and where collaboration would provide the greatest leverage, such as a high‑emission material with a concentrated supplier base or a logistics lane shared with peers. In this case, procurement plays a central role. At the ecosystem level, firms can join or initiate industry collaborations that match their key categories and geographies. Companies can push for convergence in data requests, co‑fund supplier training and audits, and explore shared financing mechanisms that help Small and Medium-sized Enterprise (SME) suppliers upgrade equipment or switch to lower‑carbon inputs.

Ultimately, the companies that will meet their Scope 3 targets are those that reframe their approach from a compliance burden into a strategic capability built on collaboration. By aligning expectations, pooling demand, and investing in supplier capabilities together, they can turn a fragmented system into a coordinated decarbonization effort, one that delivers not only emissions reductions, but also resilience, innovation, and long‑term competitive advantage.

References

CDP Worldwide. (2025). Technical Note: Relevance of Scope 3 Categories by Sector (Version 3.0). CDP. https://cdn.cdp.net/cdp-production/cms/guidance_docs/pdfs/000/003/504/original/CDP-technical-note-scope-3-relevance-by-sector.pdf?1649687608

Velázquez Martínez, J. C., Rajagopalan, S., Arnold, V. & Mora Quinones, C. A., (2025, October). State of supply chain sustainability 2025. MIT Center for Transportation & Logistics and Council of Supply Chain Management Professionals. https://sustainable.mit.edu/sscs-report/

About the authors

Dr. Sreedevi Rajagopalanis director of the MIT Sustainable Supply Chain Lab and a research scientist at the MIT Center for Transportation and Logistics. She can be reached at [email protected].

Tori Arnold is the Project Manager of the MIT Sustainable Supply Chain Lab and can be reached at [email protected].

SC

MR

More Supply Chain Sustainability

- PepsiCo moves its startup sustainability program from pilots to operational scale across Asia Pacific

- Align AI adoption with climate goals

- Sustainability and AI: A complicated and often overlooked relationship

- Why Scope 3 demands collaboration—not just compliance

- Building globally resilient value chains for sustained operations

- More Supply Chain Sustainability

Explore

Explore

Topics

Procurement & Sourcing News

- Why companies blame the wrong supplier … and miss the real failure

- NextGen Supply Chain Conference unveils agenda focused on AI, execution and the future of leadership

- From fragmented negotiations to coordinated negotiation performance: an AI-enabled approach

- Supply chain resilience isn’t a data problem; it’s a judgment problem

- Why your supply chain risk management plan will fail

- When component verification becomes operational

- More Procurement & Sourcing

Latest Procurement & Sourcing Resources

Subscribe

Supply Chain Management Review delivers the best industry content.

Editors’ Picks